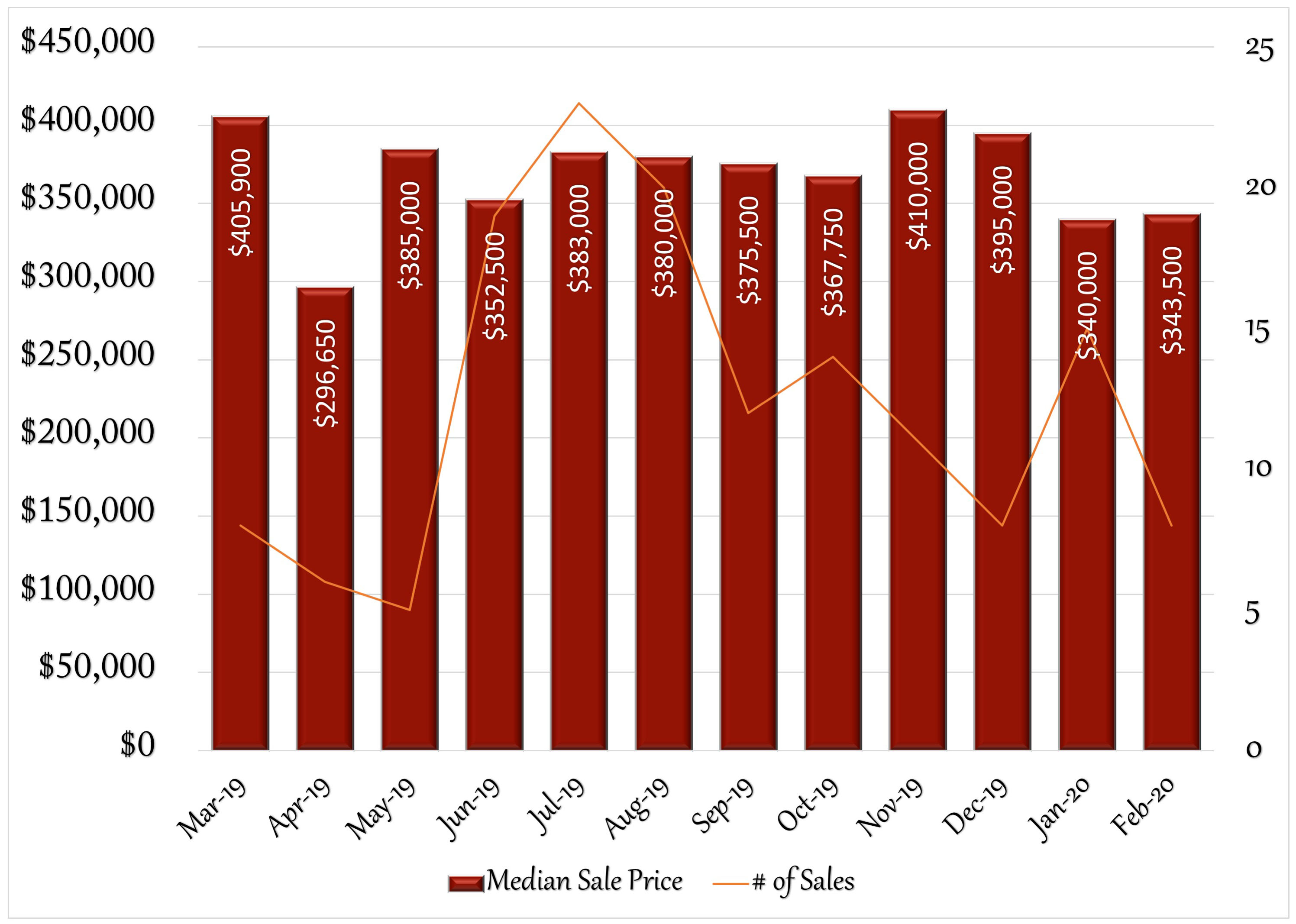

February saw another fairly stable month in the real estate market for Orange. The Median sales price was virtually unchanged, at $343,500, a 1% increase from January. There was a slowdown in the number of houses sold, from 15 in January to 8 in February, and an increase in the number of days on market (78-95), but the number of houses to be offered for sale increased from 13 to 20, and the number of active listings remained consistent with previous months. The months of supply also remained about the same; 3.4 months in January to 3.3 months in February. That means that considering the current inventory of homes, the demand from buyers is high, and Orange continues to be in a sellers-market for well over a year. Interest rates continued to drop. By months end, the 30-year fixed rate was 3.45%. This is a fantastic time to refinance higher rates or refinancing from a 30-year mortgage to a 15 year, which could save thousands of dollars over the life of a loan. Do you know anyone looking for more information about their real estate market? I’d be happy to help.

12 Month Sales Activity

Housing Stats

(change from previous month)

| Median Sale Price: | $343,500 |

| change: | 1.03% |

| YTD change: | 1.03% |

| Units Sold: | 8 |

| change: | -46.67% |

| Active Listings: | 43 |

| change: | 2.38% |

| New Listings: | 20 |

| change: | 53.85% |

| Days on Market: | 95 |

| change: | 21.79% |

| Months of Supply: | 3.30 (Seller's Market) |

| change: | -2.94% |

February Single-Family Home Sales

(OLP: original list price • LP: list price • SP: sale price • DOM: days on market)

| Address | Style | sq ft | BR | BA (f/h) | OLP | LP | SP | SP/OLP | DOM |

| 955 Corn Cob Lane | Ranch | 1,664 | 3 | 2/0 | $329,900 | $329,900 | $340,500 | 103% | 9 |

| 1075 Orange Center Rd. | Cape Cod | 4,235 | 5 | 2/0 | $370,250 | $350,000 | $346,500 | 94% | 116 |

| 359 Demarest Dr. | Ranch | 3,098 | 3 | 2/1 | $459,000 | $459,000 | $452,000 | 98% | 74 |

| 826 Sheffield Rd. | Ranch | 2,068 | 3 | 2/0 | $289,900 | $289,900 | $275,000 | 95% | 7 |

| 375 Smith Farm Rd. | Ranch | 1,472 | 3 | 2/0 | $339,900 | $314,900 | $311,500 | 92% | 183 |

| 287 Old Tavern Rd. | Colonial | 3,478 | 4 | 3/1 | $439,900 | $390,000 | $365,000 | 83% | 144 |

| 715 Cranberry Lane | Raised Ranch | 2,512 | 3 | 3/0 | $259,900 | $259,900 | $259,000 | 100% | 28 |

| 466 Yellow Brick Rd. | Colonial | 3,354 | 4 | 3/1 | $489,000 | $459,900 | $435,000 | 89% | 180 |

| Units Sold: 8 | $355,075 | $339,950 | $343,500 | 94% | 95 |

Sales Trends: January-February

Remember Tax Breaks When Selling:

Selling a home often provides the seller with certain tax deductions that shouldn’t be forgotten. One of the biggest available is the selling costs. As long as the costs are directly tied to the sale of the home, they qualify for tax breaks. Also, sellers who have lived in their home as their principal residence for at least two out of the five years prior to selling it can earn tax advantages. “You can deduct any costs associated with selling the home—including legal fees, escrow fees, advertising costs, and real estate agent commissions,” says Joshua Zimmelman, president of Westwood Tax and Consulting in Rockville Center, N.Y. But tax experts warn that these costs can’t be deducted like mortgage interest. They are subtracted from the sales price of the home. That turns into a capital gains tax. Other potential deductions for sellers are home improvement and repair costs. Sellers who made renovations to make their home more marketable may be able to deduct those costs from their taxes. Renovation projects could include painting the house or repairing the roof or water heater, for example. “If you needed to make home improvements in order to sell your home, you can deduct those expenses as selling costs, as long as they were made within 90 days of the closing,” Zimmelman says.

How To Instantly Improve Your Credit Score:

The higher your credit score, the better your chance to snag a lower mortgage rate and potentially save tens of thousands of dollars over the life of a loan. But one missed payment or a default can instantly bring a credit vscore down. “Depending on your credit history, a 15- or 20-point shift could mean the difference between being approved or declined or better terms or higher costs,” Rod Griffin, the director of public education at Experian, told CNBC. The top way to increase your credit score: Pay your bills on time and reduce your credit card balance. That habit alone can improve a score as quickly as within a few billing cycles. “As a rule of thumb, you could see an appreciable difference in six months,” Ted Rossman, an industry analyst at CreditCards.com, told CNBC. However, “if a missed payment has dragged your score down, your score could rebound in a month or two; a series of late payments will take longer to make a full recovery,” Griffin adds. The recovery for a late mortgage payment can take about nine months for a credit score to recover. Filing for bankruptcy could take up to five to 10 years. The overall credit history of the borrower plays a significant role in how fast they can recover from financial mishaps, Griffin told CNBC. But “the better your scores are to start with, the more difficult it is to improve them,” he adds. A lower credit score reflects a pattern of missed payments so adding one more missed payment isn’t as significant. But a person with a clean credit report who misses a payment will see a bigger impact, Miron Lulic, founder and CEO of SuperMoney, told CNBC. However, the goal needn’t be a perfect score, but “the goal is to have a score that qualifies you for the best terms of rates, generally 750 or above,” Griffin says. Overall, credit scores recently have been at an all-time high, ranging from 300 to 850.